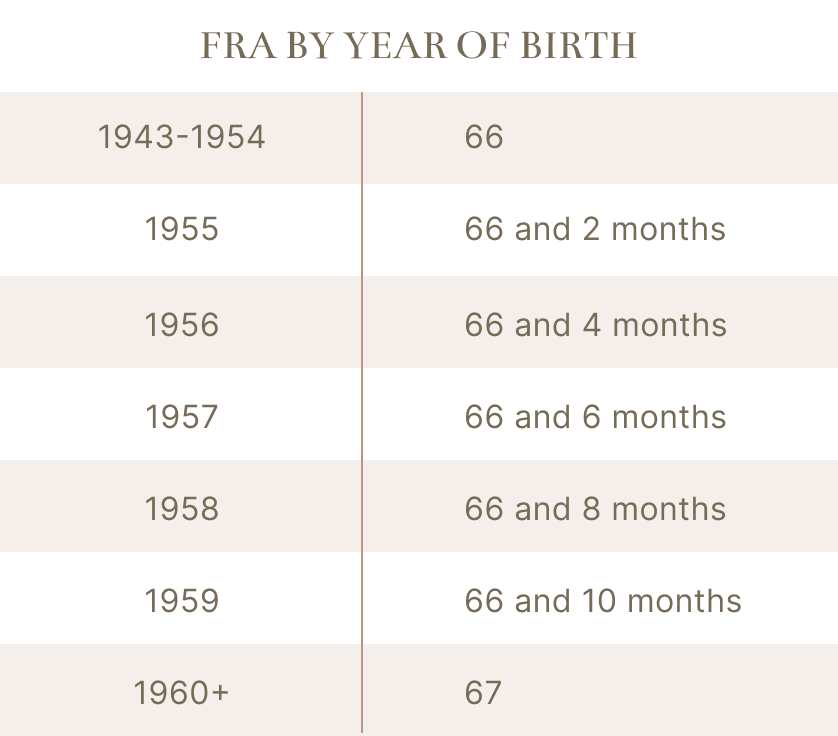

66-67 years old

Full Retirement Age (FRA) for Social Security is based on the year in which you were born. Assuming you’re not receiving a retirement or disability benefit yet, in the month following your attainment of FRA, you’re eligible to collect your full retirement benefit.

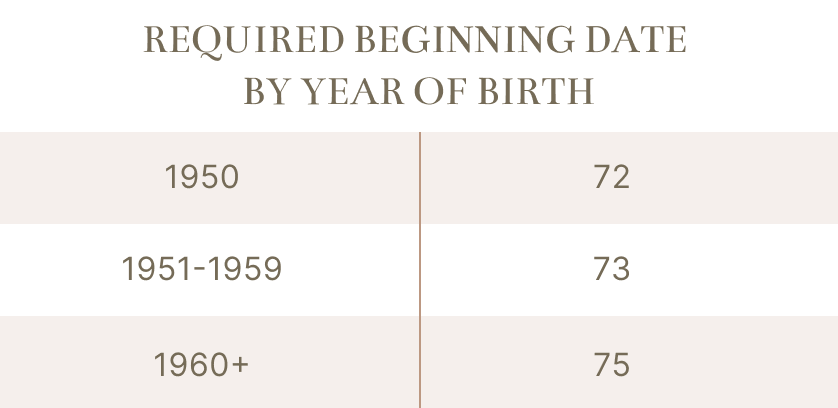

72-75 years old

The year in which you reach the required beginning date is referred to as the “first distribution year” and required minimum distributions (RMDs) from qualified accounts must begin. The IRS allows the first RMD to be postponed until April 1 of the year following the “first distribution year.” Subsequent RMDs are due by year end of each year.